Peter Souleles B. Com. LLB.

Putting Things in Perspective

Putting Things in Perspective

China has 1,054 tonnes of gold. So what? With a population of 1,336,260,000 people, that equates to 0.78 grams per person. You need three times that amount for just one wedding band. Just to give you an idea of how ridiculous their holding is, it should be pointed out that debt ravaged Greece with its 112.4 tonnes has the equivalent of 9.98 grams per person or 12.79 times more than China. In fact China would have to buy an additional 12,282 tonnes of gold just to match a bankrupt Greece. The market value of this additional purchase would be over $440 billion. If China wanted to match the USA on a per capita basis (presuming there is any gold in Fort Knox) it would have to purchase over 34,000 tonnes and pay over $1.2 trillion.

China also has $2.3992 trillion in foreign exchange reserves. Now that is a truly astounding figure until you realize two things. Firstly, this equates to only $1,795 per person. Secondly, the largest allocation is in dollar denominated assets. Whilst the standard of living in China is climbing in leaps and bounds it should be kept in mind that the improvements are off a very low base and secondly they are quite unevenly distributed.

The Problem

The point to the above is not to belittle the gargantuan size and progress of the People's Republic of China. It is to point out how futile it would be for China to aspire to a quick, visible or meaningful increase in its gold holdings by entering the market with its bulging wallet sticking out of its back pocket.

China produces around 300 tonnes of gold a year locally. There is little doubt that the bulk of this disappears into its holdings unnoticed. There is also little doubt that China is still buying gold on the international market in quantities and through intermediaries designed to not attract attention.

What is almost certain is that it will be a long time before China announces its gold holdings again. The last announcement sent a telegraphic surge through the gold market's pulse and they are unlikely to want to repeat that effect.

The irony in all this is that neither China nor the USA is going to be open and frank about their gold holdings but for totally opposite reasons. China wants to conceal its build-up of gold reserves whilst the USA is probably trying to conceal its run-down of reserves. It's a funny world.

In view of the above China will accumulate gold quietly, slowly and at the times of its choosing. It is not improbable that China is adding anywhere up to 500 tonnes per annum to its gold stockpile. If we knew this for a fact, the price of gold would shoot up. Instead, China keeps its mouth shut and enjoys a lower acquisition price. The rest of the gold community gets depressed and allows itself to be played by the manipulators.

The Bigger Problem

In the meantime, Yi Gang who is the Director of the State Administration of Foreign Exchange in China stated that "China's investment in the treasury bonds of the U.S. is based upon market behavior and should not be politicized." Now this man is no fool, but politics and investment on that scale are inextricably woven and connected and therefore unavoidably become politicized. There are serious ramifications if the delicate balance between the two is disrupted.

China has kept its currency peg to the US dollar largely in place for a number of reasons which have been identified on numerous occasions. In a nutshell this pegging basically allows China to continually feed off the US consumer whilst holding the US economy and therefore the United States to ransom. That is the macro view of the relationship. On a micro level we witness slight variations in the exchange rate as well as the level of purchases or sales of US paper when it wants to send subtle messages. At other times, it either allows Geithner to be ridiculed by Chinese University students or switches to pronouncing the importance of the US/China relationship.

While China can find nations that will accept US dollars for the payment of oil, resources as well as income producing assets such as gold mines, land etc it will keep the dollar alive in what is potentially a dangerous game of pass the parcel. The pegging though serves another purpose apart from exchange rate advantages vis-a-vis other export nations by allowing it to conceal the damage being done to the value of its holdings of US denominated assets. Had China allowed its currency to float freely, the game would be over. At the same time China's financial infrastructure is not quite ready to deal with such a scenario.

China is too calculating and is constantly shifting its position and shape to achieve its end goals. For example, the LA Times recently reported:

"China isn't buying trophy properties that might incite anger from the American public. It's also using local American partners, in order to provide even further political cover.

The largest Chinese investments in the U.S. have come from state-owned firms, primarily a $300-billion fund known as China Investment Corp. It initially targeted well-known financial companies, spending billions to buy stakes in private equity giant Blackstone Group and investment bank Morgan Stanley.

But after getting burned by the financial crisis that emerged in 2008, the sovereign wealth fund has been shifting to real estate. Its investments in the last year have included hundreds of millions of dollars in real estate-related funds managed by Oaktree Capital of Los Angeles, Goldman Sachs Group Inc. and BlackRock Inc."

The Cunning Excuse

China could easily have made an announcement up front to eliminate the possibility of it buying the remaining gold offering from the IMF. It refrained from doing so, so as to watch the market first inflate and then deflate through depression. When it finally announced that it would not buy, the following snippet appeared in Bloomberg's:

March 9 (Bloomberg) - Gold is "unlikely" to be China's primary investment to diversify its reserve holdings because of price risks, Yi Gang, head of the State Administration of Foreign Exchange, said today.

The "gold price has had handsome gains in recent years," Yi said at a briefing in Beijing today. Still, "if we look at the past 30 years, it had big ups and downs."

To not purchase the IMF's parcel on the basis of price risks is laughable, particularly when the dangers of holding US paper and Euros are far greater. This also begs the question as to why they bother buying their own local production of gold? Once again, Mr Yi is not stupid, he is simply making an announcement that suits the behind the scenes efforts and aspirations of his nation. Finally, Yi Gang states that gold is unlikely to be the PRIMARY investment. This simply means that gold will nevertheless continue to be on their shopping list.

Conclusion

Gold is the ultimate asset but does not exist in a vacuum. For this reason, readers must be constantly sensitive to any information as well as any movements that China makes in relation to Treasury Note purchases and sales, its stranglehold on rare earth metals, its constantly improving relationships and trade flows with various nations, its own internal surging demand but also lopsided investments and finally the fate of the European Union. If the Euro bites the dust maybe the purchase of gold might not seem so risky after all.

China is still slowly stripping the USA at its leisure. Only recently, the Chinese Commerce Minister Chen Deming called on the US to loosen high-tech exports to China to bridge the trade gap. What can I say? If past performance is any indication of future performance, the USA is more likely to find itself in the gap rather than bridging it.

In the meantime we lesser mortals will be entertained by two gladiators (the US and China) engaging in a game of cat and mouse in the economic and financial arena's of the world. During the intermissions in this game make sure you buy a little gold and silver.

PETER SOULELES B. Com LLB Sydney Australia 10 March 2010

The concept of entropy is one of the most useful terms for understanding just about everything. While it has its origins in natural law - thermodynamics, specifically - the concept holds true pretty much across all closed systems.

The concept of entropy is one of the most useful terms for understanding just about everything. While it has its origins in natural law - thermodynamics, specifically - the concept holds true pretty much across all closed systems.

I have a major announcement to share with you. We are launching a very big new business - a bank. I'd always thought publishing was a great business... but I've found something much, much better - banking!

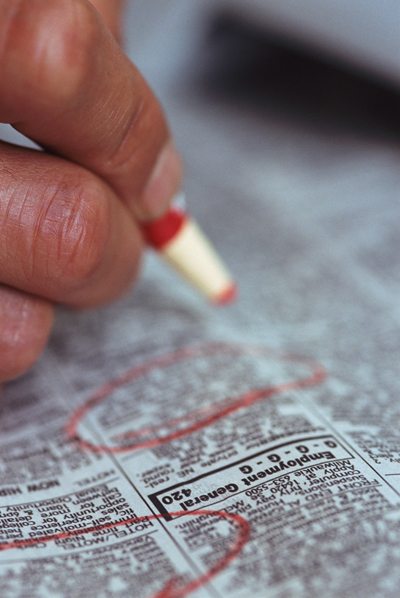

I have a major announcement to share with you. We are launching a very big new business - a bank. I'd always thought publishing was a great business... but I've found something much, much better - banking!  If employment is inversely proportional to oil prices (it is), and oil prices are only going to trend up...then employment by necessity is going down. Because oil is so fundamental to our economy, oil price increases ripple through the entire economy.

If employment is inversely proportional to oil prices (it is), and oil prices are only going to trend up...then employment by necessity is going down. Because oil is so fundamental to our economy, oil price increases ripple through the entire economy.

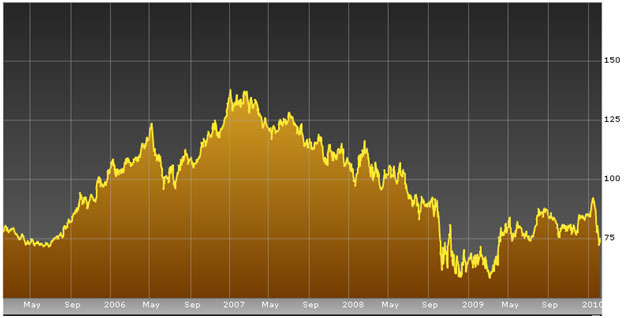

Well, the train is pulling out of the station. Gold has said goodbye to the $1,000 level and is off for northern climes. It is not your last chance to get on board, but it is your last chance to get on board at these low, low prices. The hard analysis of the past few months has been identifying the intermediate bottom, but now that that is in it is time to step back and once again focus on the big picture. Friday's Wall Street Journal has an excellent article on unemployment and the "minimum wage" law, and this is a very good time to discuss this most important subject.

Well, the train is pulling out of the station. Gold has said goodbye to the $1,000 level and is off for northern climes. It is not your last chance to get on board, but it is your last chance to get on board at these low, low prices. The hard analysis of the past few months has been identifying the intermediate bottom, but now that that is in it is time to step back and once again focus on the big picture. Friday's Wall Street Journal has an excellent article on unemployment and the "minimum wage" law, and this is a very good time to discuss this most important subject.  In these articles, I try to present an economic overview so that you can get an appreciation for the massive irrationality and ignorance of facts which pervades our society on the subject of economics. For people who already understand this and are looking for specific advice on how to protect yourself (and profit) from the dishonest policies of our government, I publish a fortnightly (every two weeks) newsletter which gives specific buy and sell signals and discusses tactics (such as whether you should be in gold or gold stocks, and what kinds of stocks). This newsletter is The One-handed Economist, and the cost is $300 per year. (It has proven a very good investment for subscribers over the past 10 years). You may subscribe either by going to my web site,

In these articles, I try to present an economic overview so that you can get an appreciation for the massive irrationality and ignorance of facts which pervades our society on the subject of economics. For people who already understand this and are looking for specific advice on how to protect yourself (and profit) from the dishonest policies of our government, I publish a fortnightly (every two weeks) newsletter which gives specific buy and sell signals and discusses tactics (such as whether you should be in gold or gold stocks, and what kinds of stocks). This newsletter is The One-handed Economist, and the cost is $300 per year. (It has proven a very good investment for subscribers over the past 10 years). You may subscribe either by going to my web site,

DI CLIFF KINCAID

NewsWithViews.com

Il New York Times cita un portavoce di George Soros che dice che il famoso operatore di hedge fund non è colpevole di alcun illecito in relazione allo sconvolgimento finanziario che sta attualmente coinvolgendo la Grecia e l’Europa nel suo insieme. Ma Zubi Diamond, autore del poderoso nuovo libro,

DI CLIFF KINCAID

NewsWithViews.com

Il New York Times cita un portavoce di George Soros che dice che il famoso operatore di hedge fund non è colpevole di alcun illecito in relazione allo sconvolgimento finanziario che sta attualmente coinvolgendo la Grecia e l’Europa nel suo insieme. Ma Zubi Diamond, autore del poderoso nuovo libro,