Warning Signs Of Full Spectrum Collapse Are Everywhere Giordano Bruno

The sovereign debt crisis in Greece and many other European nations has, at least for the moment, opened a gap in the wash of financial disinformation that has prevailed in the mainstream media for the past year. The average American is now more aware of the terrible costs of living in an artificially driven and widely manipulated “global economyâ€, and has also been exposed (at least for the moment) to the very real frailties in our own markets, which have been hidden or downplayed by the government as well as disingenuous establishment economists. Events in the EU, however, are only a glimpse of the greater and more imminent threats we face in the near future. In this article we will look at some of the latest and most disturbing moves by governments and financial institutions, as well as tell-tale signs in our own local cities, which signal that a full-spectrum collapse of world markets and possibly our own currency is not only in progress, but nearing completion.

The sovereign debt crisis in Greece and many other European nations has, at least for the moment, opened a gap in the wash of financial disinformation that has prevailed in the mainstream media for the past year. The average American is now more aware of the terrible costs of living in an artificially driven and widely manipulated “global economyâ€, and has also been exposed (at least for the moment) to the very real frailties in our own markets, which have been hidden or downplayed by the government as well as disingenuous establishment economists. Events in the EU, however, are only a glimpse of the greater and more imminent threats we face in the near future. In this article we will look at some of the latest and most disturbing moves by governments and financial institutions, as well as tell-tale signs in our own local cities, which signal that a full-spectrum collapse of world markets and possibly our own currency is not only in progress, but nearing completion.

World Market Signals

All eyes have been focused on the Greek situation for the past month, but we cannot let this one storm of the financial crisis distract us from the other threats that lie just beyond the horizon. There are many far more pressing concerns than insolvency in Southern Europe, though we’ve been drowning in “Greek Contagion†rhetoric 24/7 and it is difficult to think of much else. The idea that instability in Greece is somehow responsible for instability in the rest of the EU is simply unfounded. Most nations in the EU were on the verge of bankruptcy long before the sovereign debt crisis in Greece began. Spain, for instance, has just lost its AAA credit grade with Fitch Ratings due to its massive deficits:

http://www.bloomberg.com/apps/news?pid=20601087&sid=aqiS_6hwClPg&pos=1

Italy, Ireland, and the UK are likely not far behind. The UK posted record deficits in April:

http://www.bloomberg.com/apps/news?pid=20601068&sid=a3CziXMGujDA

Their government has recently called for budget cuts which could target some welfare, unemployment, and disability payouts in order to blunt the edge of their own growing debt problem. Some say this move is too little too late, and that Britain may have to face the same austerity measures as Greece just to survive:

http://www.marketwatch.com/story/uk-budget-cutting-begins-with-83-billion-slice-2010-05-24

There are two problems with the news coming out of the EU. First, establishment economists will attempt to dilute public awareness of the issues by diverting all blame to the Greek crisis. By making claims of Greek contagion, they give the masses the false impression that stopping the fallout in Greece will somehow cure the systematic meltdown in the rest of the world. Already, euro-zone economists (propagandists) are feeding the Greek people the same lie as our economists have been feeding us, declaring that a weak currency and import capability, combined with greater reliance on other nations and the IMF, will create some kind of ‘export nirvana’, and that Greece will suddenly rise from the grave as a kind of industrial powerhouse:

http://www.reuters.com/article/idUSTRE64G11U20100517

This is the same double-think the globalists have been using everywhere; “Weakness is strengthâ€.

Regardless of what talking-head financial analysts tell us in the next six moths, we must never forget that the collapse was not caused by a single nation, but the actions of all governments in collusion with international banks over a period of decades.

Second, we will be hearing a lot in the news over the coming year about the credit grades of rating companies such as Fitch or Moodys. However, these credit grades are a purely psychological affair. If they were based on concrete fundamentals, Spain would have lost its AAA credit rating long before now, not to mention the UK or the U.S. The fact that they are finally willing to begin downgrading the debt value of certain countries only shows that circumstances have become so untenable that rating agencies know they will look foolish if they do not do otherwise. Now that they have begun, watch for rating downgrades to accelerate in the coming year, especially in the EU, punishing the markets with repetitive stock plunges.

The biggest news, though, the news that no one is paying much attention to, is the activity in Asia. In the midst of all the chaos across the Atlantic, we have forgotten to take note of the activities of the great elephant in the room just across the Pacific.

China has been busy, and the speed at which they are shifting their economic system is even startling. In past articles we covered the Chinese dumping of U.S. Treasury Bonds in response to our ever rising national debt and dangerous liquidity measures by the private Federal Reserve. All this, we believed, was in preparation for a valuation of the Yuan and a decoupling of the traditional trade relationship between China and America.

To be clear, some economists have begun overstating the recent purchases of new T-bills by China in response to the European debt crisis. Meaning, they believe China will now turn back to the Dollar as a safe haven asset against a fall in the Euro. China has only increased its reserves by 2% in response to the possibility of a Euro collapse, which in my opinion is hardly a show of faith in the Dollar. Also, the vast majority of purchases in recent months have been for SHORT TERM treasury bonds maturing in 26 weeks or less. You can see the chart for all April purchases here:

https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEh1B7EhlBG635jXe0D9Mdp0b187YbCaCd1r70fPGknF6tuP4-oTt0nUrdhsnGvBIlZMwdq1jJ3vzpa17A5j6Gdjv9ClpA33uL58mSe8QzKoQp-Fi3vINv_kcyjC-TqlLf12sIcG8QaK_JQ/s1600/Apr10-Auction.JPG Countries buy short term bonds in our debt because they see our long term debt as a severe risk. With our deficits climbing to levels never dreamed of only ten years ago, we need long term investment in our Treasuries if we are to sustain the U.S. economy. These investments are not coming, nor is it probable that they will in the future. China is now ready to de-peg the Yuan from the Dollar if not break from the American financial system completely.

Back in 2008, rumor spread in some investment circles that China was planning to issue its own T-bonds; called “Panda Bonds†or “Yuan Bondsâ€:

As it turns out, Yuan Bonds are no longer a rumor. Issued late last year with little fanfare, and considered by some investors as a novelty, Chinese Treasuries are now growing far beyond expectations:

http://english.peopledaily.com.cn/90001/90778/90859/6986357.html

Even more intriguing, China has opened its index futures to foreign investors, revealing a desire to take a more central role in world economic activity:

http://english.peopledaily.com.cn/90001/90778/90862/002046.html

China has had trillions of dollars in currency reserves which help create the trade deficit that allows their industrial based export economy to thrive. Why would they want to issue bonds in their own currency, increasing the value of the Yuan and ending their trade advantage? Because China’s goal is to convert its billion citizen society into an import and consumption hub while making the RMB, or the Yuan, a reserve currency to rival the Euro and the Dollar.

Indeed, these bonds are meant to strengthen the Yuan, increase its prominence as a reserve currency, and eventually allow China to break from U.S. treasuries entirely. It is also possible that the valuation of the Yuan could make it eligible for inclusion in the IMF’s Special Drawing Rights basket currency, a goal China has openly expressed:

http://www.reuters.com/article/idUSTRE6250LC20100306

China has strengthened ties with Indian markets, African markets, and formed the ASEAN trading block. ASEAN is now attempting to “unite†with the European Union in order to “combat†the global financial crisis:

http://english.peopledaily.com.cn/90001/90777/90856/7001488.html

Every single action by China in the past two years indicates that they are not only preparing to break with the U.S., but that they are ready to do so today if they preferred. The bottom line is this: China wants reserve status for the Yuan, and China wants the Greenback replaced as the world reserve currency. When China de-pegs the Yuan from the Dollar, they will begin dumping whatever U.S. treasuries they still hold, allowing the Yuan to strengthen and the Dollar to fall. This will be a disaster for the U.S. economy, and it could conceivably happen before the end of this year.

Not far off the coast of China, Japan has found itself in dire straights. Still clinging to the traditional export relationship with the U.S., America is no longer consuming Japanese goods anywhere near the pace they were once accustomed. This has resulted in a deflationary spiral in Japan’s markets, as well as wages and wholesale prices of goods. Expect to hear much more about this before the end of 2010:

http://www.bloomberg.com/apps/news?pid=20601087&sid=a9.PG6nGY6_g&pos=5

The Japanese government has on several occasions suggested ending reliance on the U.S., and to discontinue purchases of U.S. Treasuries. They have also hinted at the possibility of fully joining China’s ASEAN trading bloc as a way to offset any damage done by breaking from American markets. The deflationary collapse in Japan is extremely hazardous and grows worse now with each passing month. Japan may soon have no other choice but to turn to ASEAN for trade support and end its relationship with the U.S. Once again, this move would bring calamity to American stocks and to our currency.

Brazil, a member of the BRIC group of nations along with China, is facing serious upheaval in its bond markets:

http://www.bloomberg.com/apps/news?pid=20601087&sid=aUVznIauvQYg&pos=4

The Brazilian currency is also declining in a fashion much like the Euro, and their sovereign debt issues are becoming unmanageable. This in turn could lead to greater pressure from BRIC nations to push for a new reserve currency outside of the Dollar and the Euro.

These signals across the globe are like the swell of the tide just before the onslaught of a hurricane. If you know how to read the waters, then you know when its time to stop the beach party and run for cover.

American Market Signals

Though the infinite stimulus by the Federal Reserve and the skewing of statistics by government agencies like the Labor Department have lead the average American to believe a recovery is in the making, the fact is, our situation has only become worse since the initial collapse began in 2007. Most recent signs indicate we may soon return to the hyper-volatility we saw in the Dow back in 2008, but this time, the Dollar will follow the plunge of stocks instead of hedging against it.

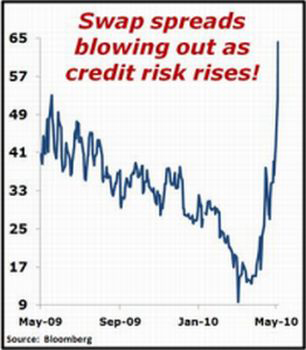

Key measurements of credit instability are once again spiking, just as they were before the Dow plummeted out of control in 2008. As you can see from the chart below, 2 year swap spreads slowly rolled above 60 basis points just before the Dow began to plunge:

This year, 2 year swap spreads have rocketed up from 9.6 basis points in March, to as much as 64 basis points in May! That’s a seven fold increase in the span of a couple of months, unlike the collapse of 2008, which saw spreads rise much slower:

Credit swap spreads rise when banks charge higher premiums. Banks charge higher premiums when they do not trust the creditworthiness of other banks. Corporate bond sales have fallen to the lowest levels in a decade:

http://www.bloomberg.com/apps/news?pid=20601087&sid=aZWveN7GJtks&pos=7 The swap spread chart is basically a red flag that goes up when banks are preparing for serious market turmoil. It seems as though that turmoil may be near due to the explosion in swap spreads in such a short period of time. You can read more about swap spreads and their warning signs here:

http://www.moneyandmarkets.com/credit-crisis-indicators-going-bonkers-again-batten-down-the-hatches-39253 The warnings behind swap spreads are substantiated by the behavior of U.S. stocks in May, which had the worst profit losses since 1940:

http://www.bloomberg.com/apps/news?pid=20601087&sid=apgUzNgFGKLA Private wages have sunk to historic lows, while government welfare payouts have risen to historic highs. This is a sure sign of an economy that is about to flop on an epic scale:

http://www.usatoday.com/money/economy/income/2010-05-24-income-shifts-from-private-sector_N.htm Mass layoffs in April also reveal a rather ironic problem. Ever since the bailouts began, establishment heads have been playing up the “advantages†of inflation, claiming that America would soon return to a stronger industrial base and that more factory jobs were on the way. However, a recent measure of mass layoffs by companies shows that widespread job cuts were led by manufacturers who shed workers even as the economy was supposedly in the midst of recovery!

This means that there is no growth in industrial jobs, and the hypothetical plans and promises of the pro-inflation crowd bear little-to-no weight in the real world.

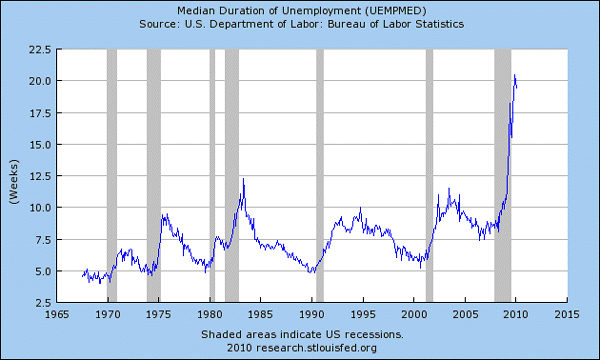

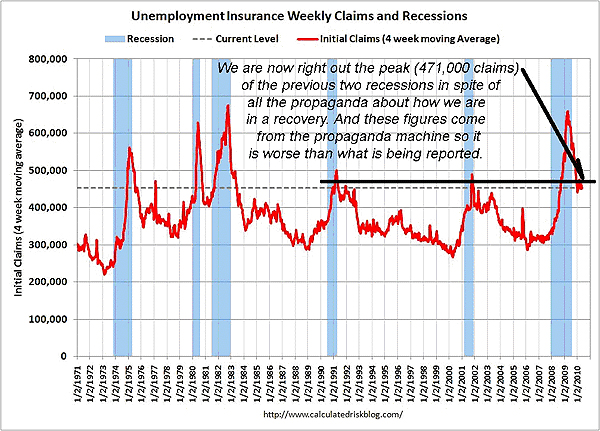

The unemployment issue is also liable to be exacerbated in the next month, largely due to the expiration of government unemployment benefits on June 2nd. The Senate is not even set to convene discussion on extensions until June 7th, after Memorial recess. The fact that they refused to handle the matter until after benefits have already expired may suggest that they do not intend to extend unemployment at all. Millions of people who have remained unemployed for long periods due to the recession could lose benefits all at once:

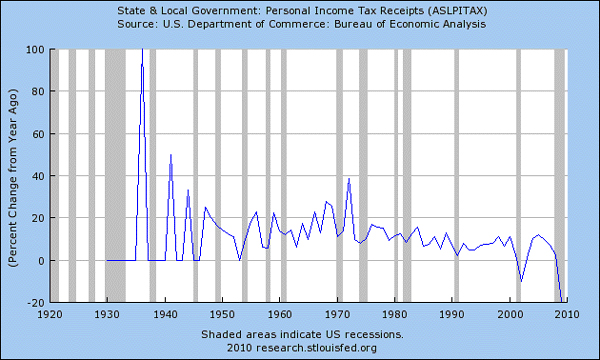

State And Local Signals

The big story in state and local markets is municipal bonds. Investment in local debt has completely dried up. States and cities across America are amassing impressive budget shortfalls in record time. California as a whole is best known for being on the verge of debt default, but little do we hear about individual towns and counties within California that are already talking about filing for Chapter 9:

http://www.time.com/time/business/article/0,8599,1991062,00.html

http://www.reuters.com/article/idUSTRE64Q6CQ20100527

California is not the only state with cities on the brink. The National League of Cities has reported that U.S. municipalities will come up short on debts to the tune of up to $80 billion:

http://money.cnn.com/2010/05/28/news/economy/american_cities_broke.fortune/index.htm According to the Economic Policy Journal, 32 states are now technically bankrupt, and are borrowing money from the Federal Treasury just to keep up with unemployment benefits:

http://www.economicpolicyjournal.com/2010/05/32-states-have-borrowed-from-treasury.html

What we are looking at appears to be a snowballing implosion of municipal funding, starting small with cities and counties one by one filing for bankruptcy until a crescendo of debt default is reached, resulting in the breakdown of state governments, making them totally reliant on fiat from the Treasury and the Federal Reserve just to function. This is yet another opportunity for hyperinflation to fester.

We might think of corporations as international and not local, but since corporate chains now dominate local economy, it is important to consider them in a local light. Municipal Bonds are not the only train wreck in progress. As we mentioned above, corporate bond markets are also now frozen. This could lead to a whole host of financing issues for corporations, not to mention even more downsizing and job losses.

Wal-Mart is one example of a major corporate chain that is ingrained into the financial root of most communities (for good or ill), and it is also an example of a chain at risk:

http://money.cnn.com/2010/05/20/news/economy/consumer_retail_walmart.fortune/index.htm

When the sales of a monstrous price undercutting consumer outlet like Wal-Mart start slipping, then we are in serious trouble.

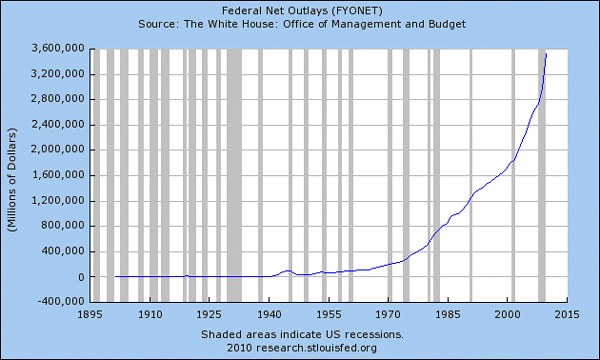

There are only two cures for the current debt landslide we are now in the midst of. States and cities could make radical cuts in spending and put new programs on hold until the crisis has passed. It is highly doubtful our government officials will suddenly take on a fiscally conservative approach at this late juncture. The only other option is to raise taxes to levels never before seen and print money out of thin air to pay off debts (the most probable scenario). Printing money does little to actually solve our insolvency issues, though. It does not remove debt, it just reallocates it. By injecting fiat into state economies and corporate banks, we only move debt from the local and state sector to the federal sector, not to mention devalue the Dollar itself. Higher taxes would also squeeze the American consumer (the lifeblood of our 70% consumer based economy) even further, ending what little chance we had left to rebuild Mainstreet.

These factors and many others that have arisen in the past 6 months do not demonstrate a financial system that is catching its breath and climbing from the depths, but one on an erratic ride tethered like a daredevil to a frayed bungee-cord; eventually, things are going to snap, and the ride will end…

It is incredibly hard to put into words the absolute horror that is happening in the Gulf of Mexico right now. The millions of gallons of oil that have gushed into the Gulf of Mexico and BP's efforts to fight the massive leak are turning the Gulf into a lifeless toxic stew of oil and chemicals. The damage caused to wildlife in the Gulf by this spill will be incalculable. Entire species are at risk of being wiped out. Scientists are telling us that the primary dispersant being used by BP ruptures red blood cells and causes fish to bleed. This is by far the greatest environmental disaster in U.S. history, and there is no end in sight.

It is incredibly hard to put into words the absolute horror that is happening in the Gulf of Mexico right now. The millions of gallons of oil that have gushed into the Gulf of Mexico and BP's efforts to fight the massive leak are turning the Gulf into a lifeless toxic stew of oil and chemicals. The damage caused to wildlife in the Gulf by this spill will be incalculable. Entire species are at risk of being wiped out. Scientists are telling us that the primary dispersant being used by BP ruptures red blood cells and causes fish to bleed. This is by far the greatest environmental disaster in U.S. history, and there is no end in sight. In 64 AD,

In 64 AD,

For more than 100 years, college has been considered a sound and desirable investment in one's financial future. But unlike other forms of investment, those contemplating dropping more than $100,000 to obtain a degree from a private university, or $28,000 for one from a public university, seldom stop to consider whether what made sense for a previous generation still makes sense today.

For more than 100 years, college has been considered a sound and desirable investment in one's financial future. But unlike other forms of investment, those contemplating dropping more than $100,000 to obtain a degree from a private university, or $28,000 for one from a public university, seldom stop to consider whether what made sense for a previous generation still makes sense today.

The BP oil spill is now recognized as the worst environmental disaster in U.S. history. It is also shaping up to be a harbinger of stagflation.

The BP oil spill is now recognized as the worst environmental disaster in U.S. history. It is also shaping up to be a harbinger of stagflation.

{kind=link}